Let’s start with step by step guidance on completing this innocent spouse relief form.

There are 7 parts to this 7-page tax form:

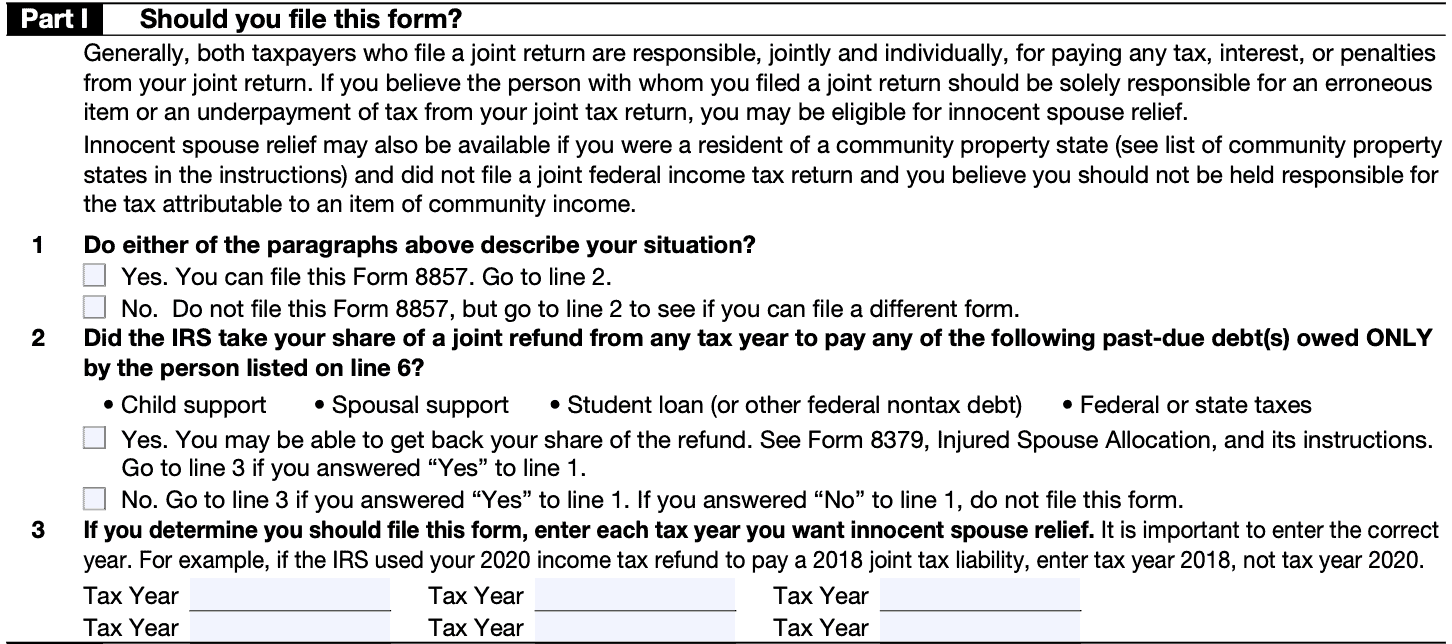

Part I of this tax form helps taxpayers determine whether they can actually use Form 8857 to claim taxpayer relief.

The top of Part I describes situations in which innocent spouse relief might be available:

If you believe the person with whom you filed a joint return should be solely responsible for an erroneous item or an underpayment of tax from your joint tax return, you may be eligible for innocent spouse relief.

Innocent spouse relief may also be available if you were a resident of a community property state and did not file a joint federal income tax return, and you believe you should not be held responsible for the tax attributable to an item of community income.

If you believe either of those statements to be true, select “Yes.” Otherwise, select “No.”

In either situation, proceed to Line 2 once you’ve entered your answer.

Did the IRS take your share of a joint refund from any tax year to pay one of the following past-due debts, owed only by the person listed on Line 6?

If Yes, you may be able to get back your share of the tax refund by filing IRS Form 8379, Injured Spouse Allocation.

Go to Line 3 if you answered “Yes” to Line 1.

If No, then do not file this form if you also answered “No” to Line 1. If you answered Yes to Line 1, continue to Line 3.

Enter each tax year that you want innocent spouse relief. Be sure to enter the correct year.

For example, if the IRS used your 2023 income tax refund to pay a 2021 joint tax liability, enter the tax year 2021, not 2023.

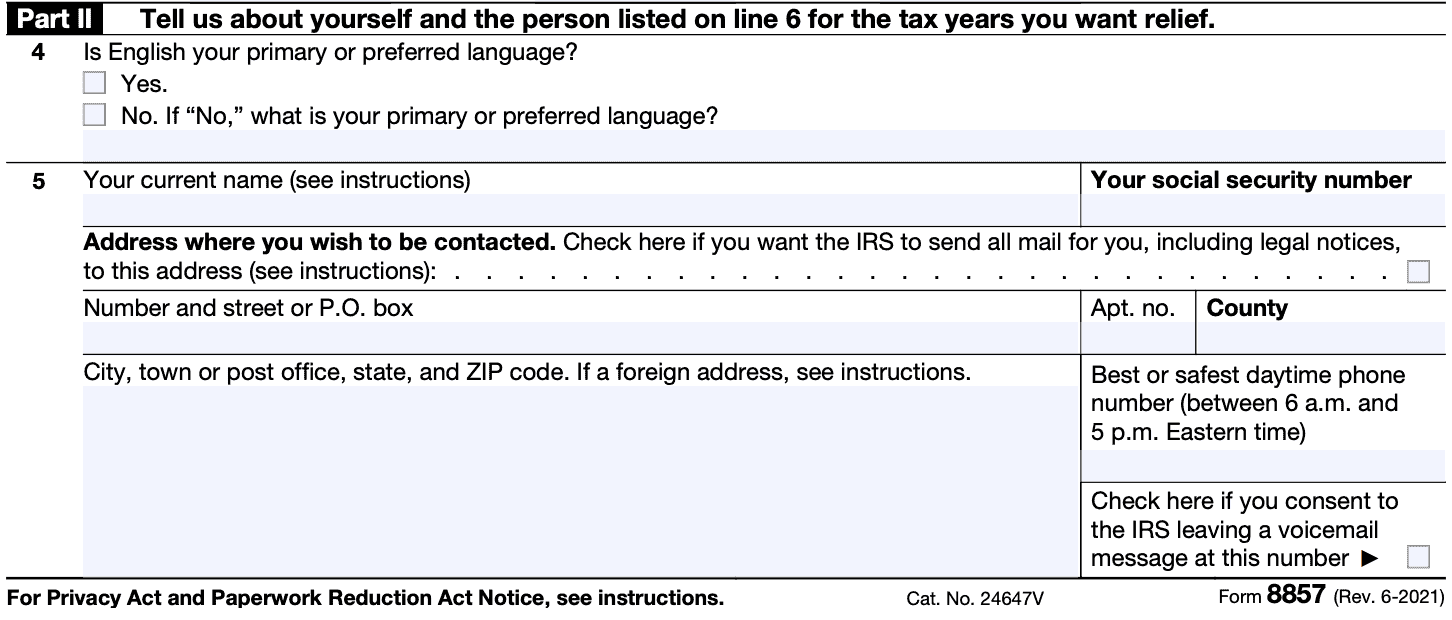

In Part II, you’ll give the IRS some personal information about yourself and the other spouse.

If English is not your primary language, then check No and indicate your preferred language. Otherwise, select Yes and go to Line 5.

In Line 5, you’ll enter your taxpayer information. This includes:

If you have an individual taxpayer identification number (ITIN) instead of a Social Security number, enter your ITIN instead.

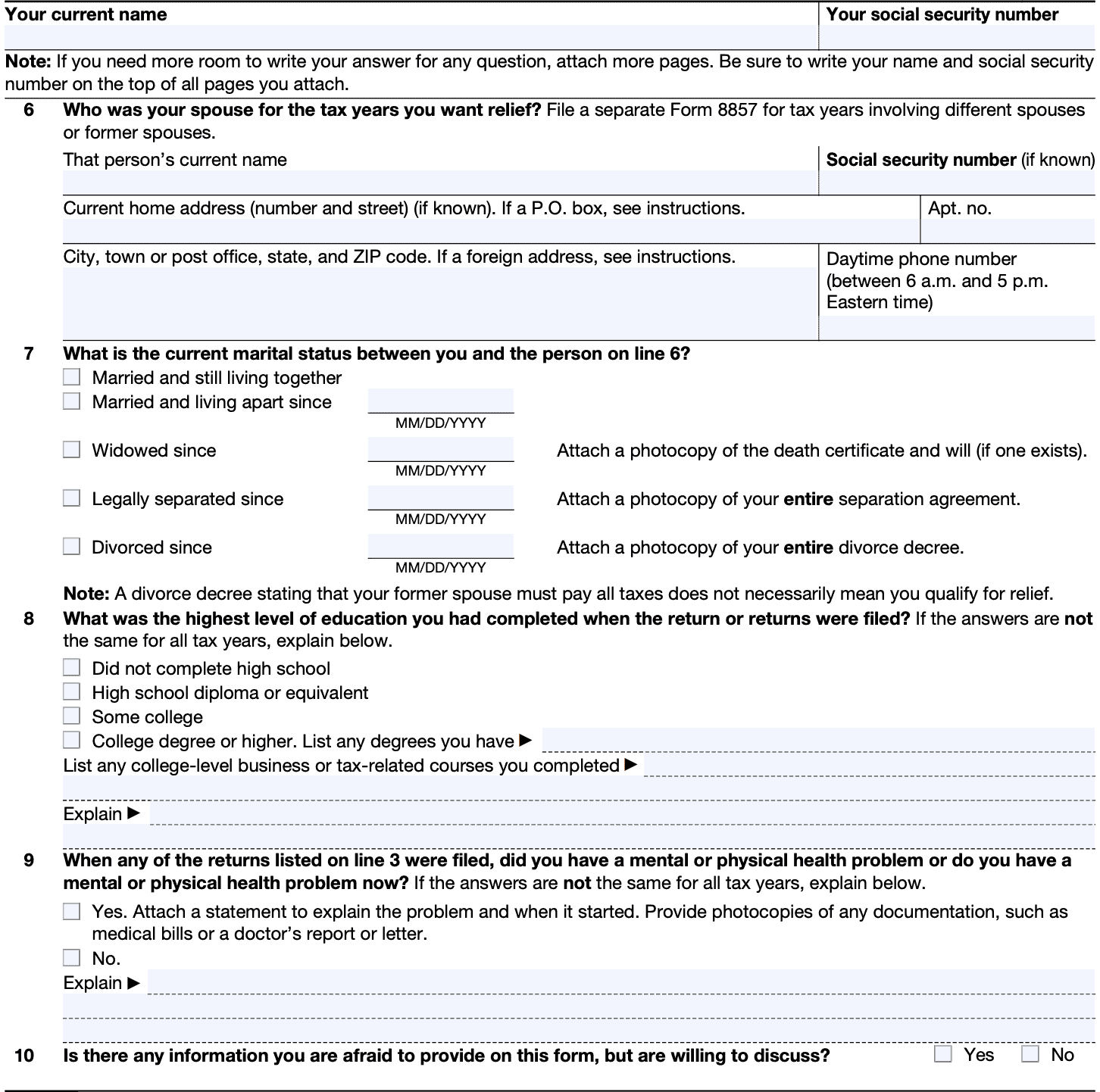

In Line 6, you’ll enter the identifying information for the spouse from whom you’re claiming relief. This includes:

Only enter a P.O. Box if you do not know the mailing address or if the postal service does not deliver mail to that address.

Enter the marital status that applies:

In Line 8, enter the highest level of formal education that you have achieved:

If applicable, enter any college-level business or tax courses that you may have completed.

If applicable, attach a statement to explain the problem. Provide copies of any supporting documentation, such as medical bills, medical record, doctor’s report, etc.

Select Yes if you have information that you cannot provide on the form, but you’d like to discuss with the IRS. Otherwise, select No and go to Part III.

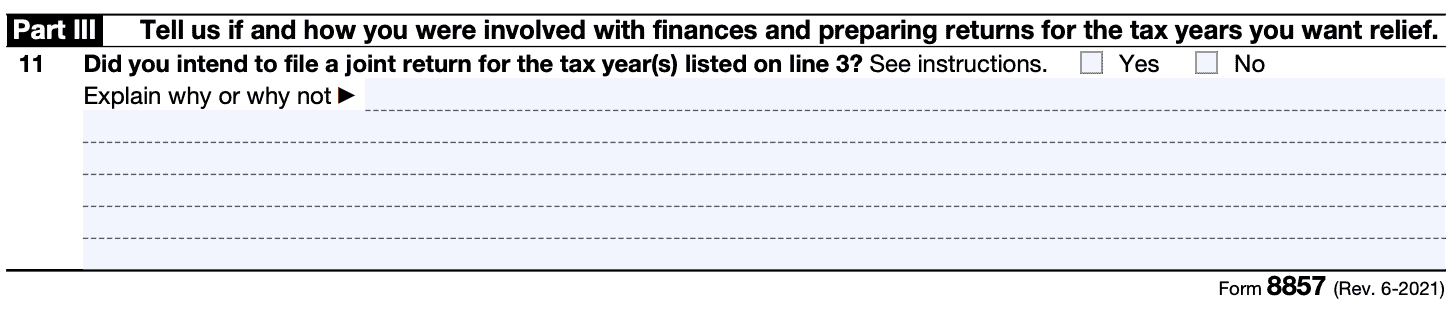

In Part III, you’ll outline your involvement, if any, in either household finances or tax preparation.

By law, if a person’s name is signed to a return, the IRS will assume that person signed the return, unless that person proves otherwise.

If you believe someone forged your signature or that you signed under duress, check Yes and explain in the space provided.

If your signature was forged or you signed under duress, the election to file jointly is not valid and you have no valid joint return. Should the IRS determine your signature was not valid, then you will be removed from the account and you will no longer be liable for any taxes owed for that return.

If the IRS determines that a valid joint return was filed, they will then consider whether you would be entitled to innocent spouse relief.

Include details such as:

Explain in the lines provided. If you need more room, attach additional pages.

To the extent possible, describe:

If you did not know, explain why you did not. If the other person was self-employed, explain whether you helped that person with maintaining books and records.

If you were aware about missing information, or whether you asked about missing or incorrect information on the tax return, please explain.

If you did not know the returns showed a balance due, explain why you did not know.

Describe any and all financial problems you may have been facing during the tax period. If there was more than one financial problem, explain all of them.

Explain whether you and the other spouse had joint accounts or separate accounts. Also explain who paid bills, made deposits, etc.

If Yes, then explain the following:

If Yes, explain. List the assets transferred, dates transferred, and fair market value on the date(s) of transfer.

If there is debt associated with an asset, explain who is responsible for the debt, how much debt was outstanding, and whether that debt has been satisfied.

Finally, explain why the assets were transferred to you. If you no longer possess the assets, explain what happened.

If the IRS determines one or both of the following, you might not be entitled to innocent spouse relief:

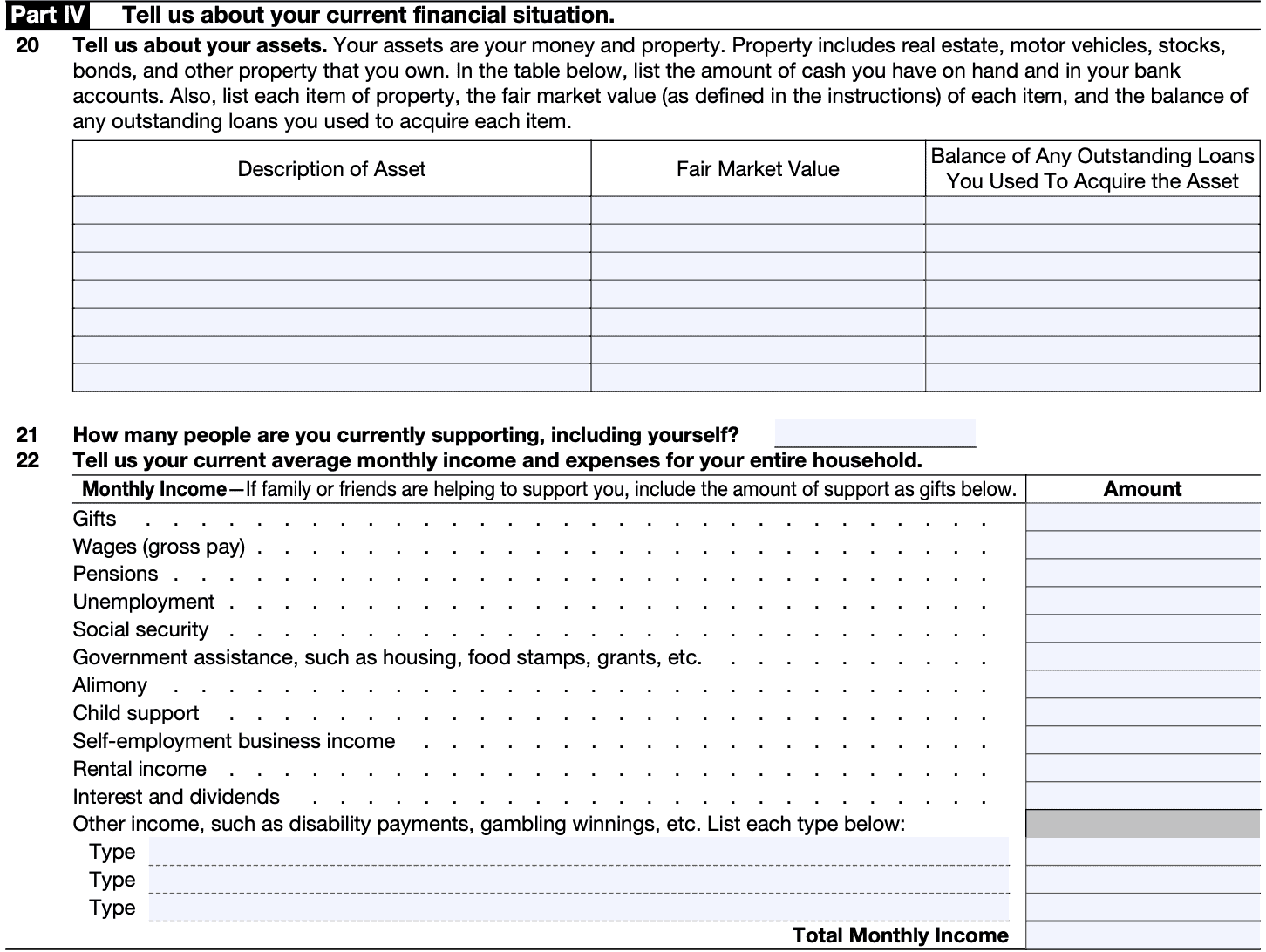

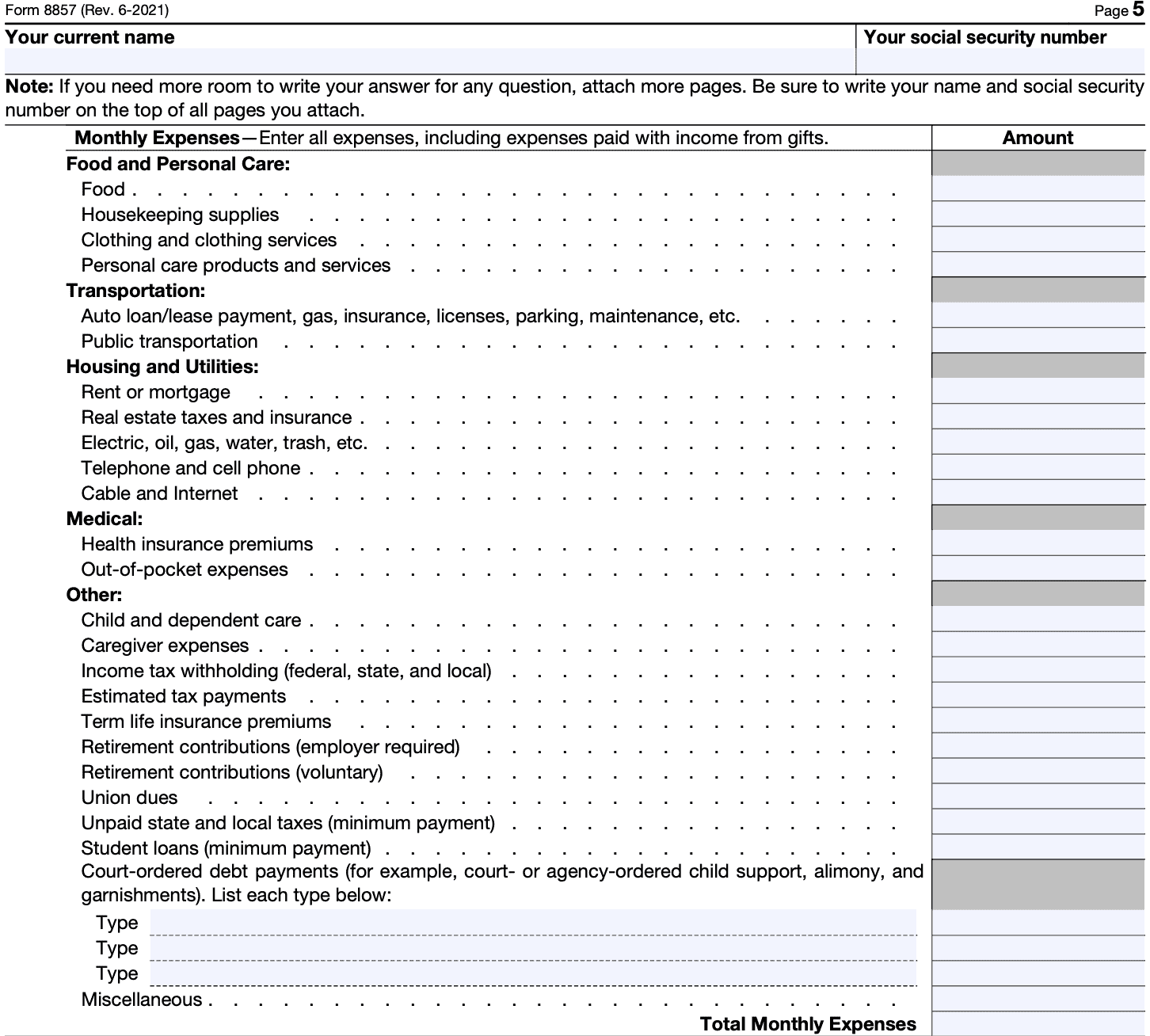

In Part IV, you’ll describe your current financial situation.

Include your assets, such as real estate, cars, investments, or other property that you own. For each item, include:

The IRS deems fair market value to be the price at which property would change hands between a willing buyer and a willing seller when both have reasonable knowledge of the relevant facts and neither has to buy or sell. This is not necessarily the replacement cost of the item.

Including yourself, how many people are you supporting on your income?

For each item, list the monthly amount in the applicable row. If you are receiving financial assistance from friends or family, then include that amount under “Gifts,” below.

current financial situation." width="1452" height="1092" />

current financial situation." width="1452" height="1092" />

Enter all expenses by monthly amount.

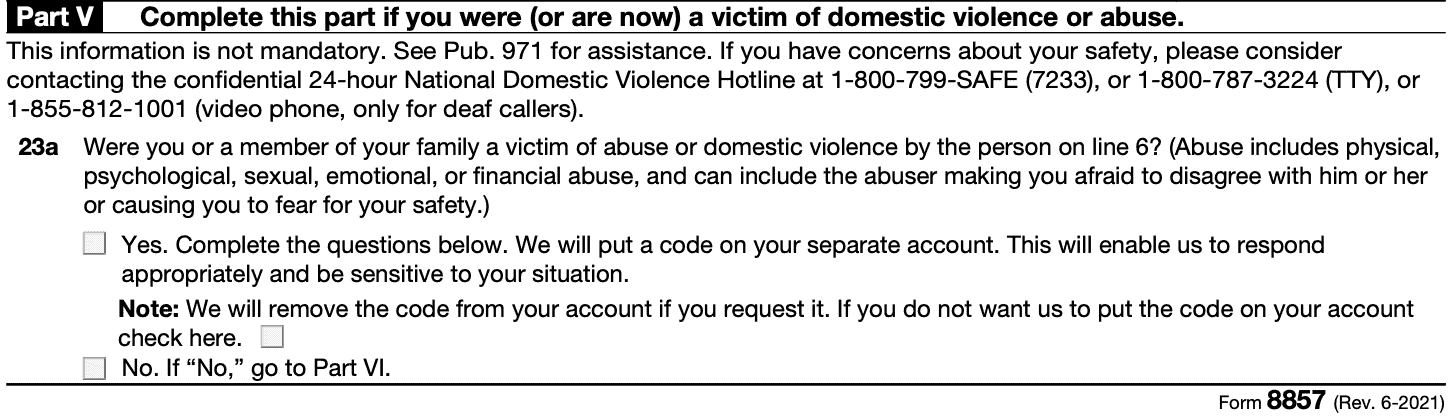

You do not have to complete Part V. If Part V does not apply, skip to Part VI, below.

If applicable, answer honestly and completely.

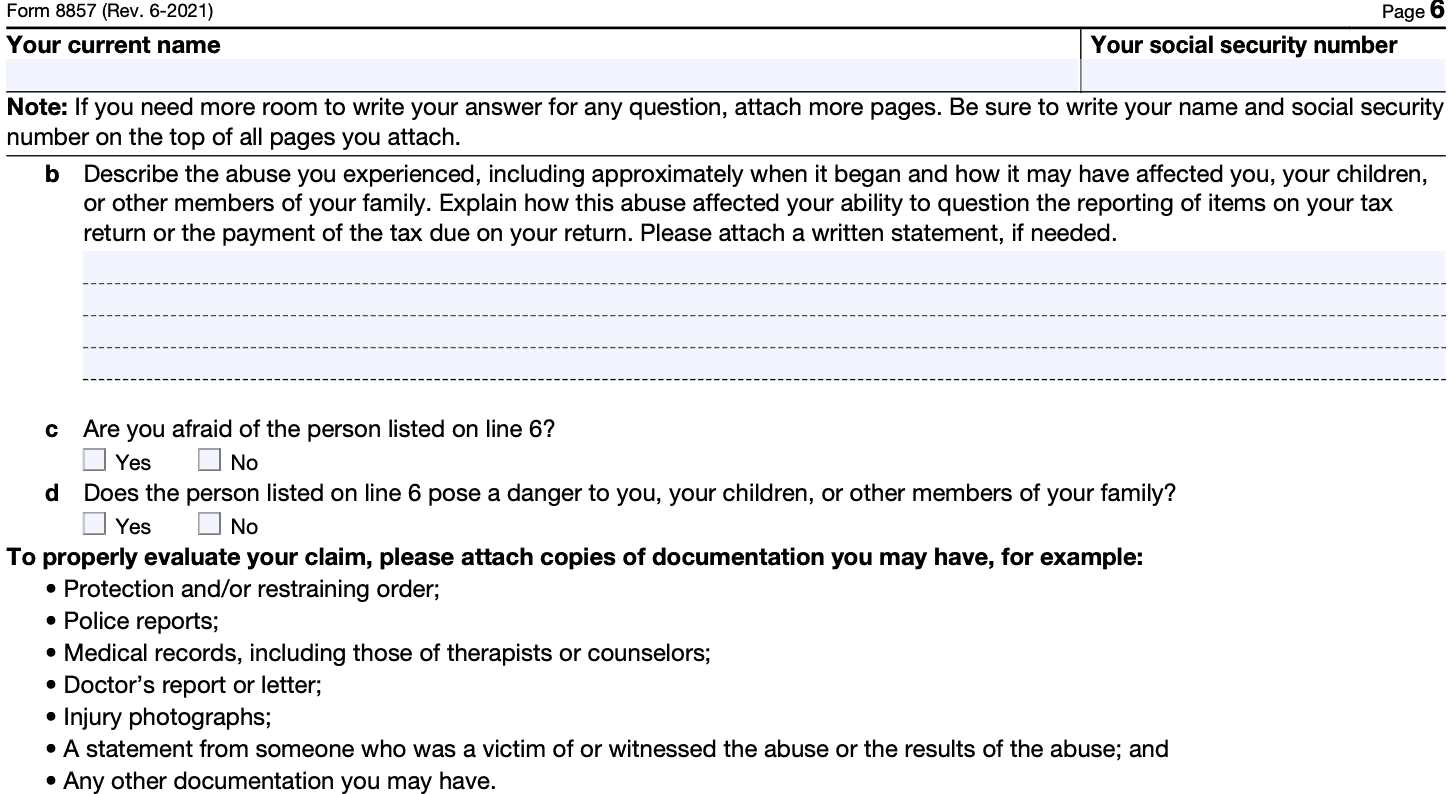

You may need to attach copies of supporting documentation, to include:

You may also consider calling the 24/7 National Domestic Violence Hotline:

Please note whether or not the person continues to pose a danger to you or your family.

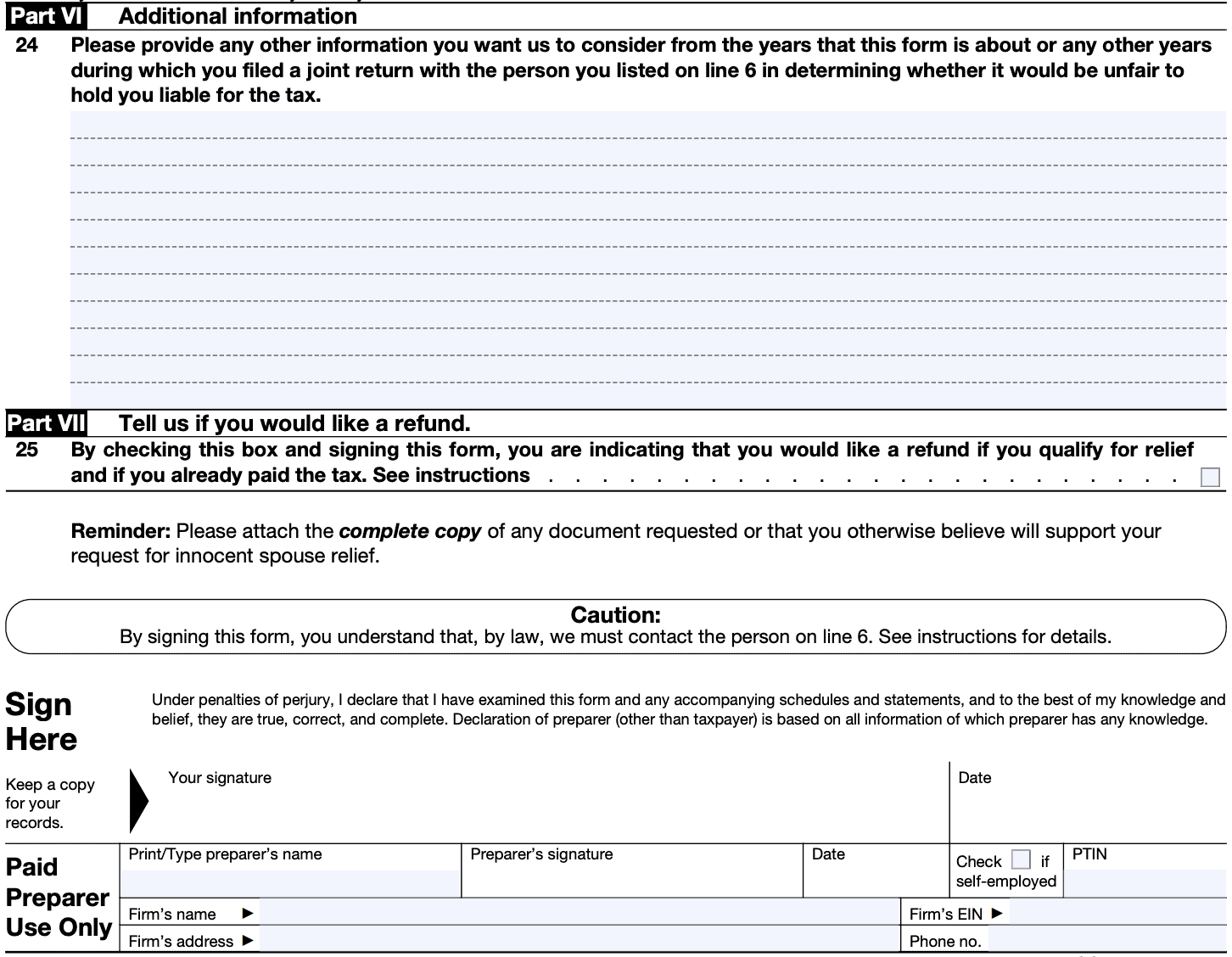

In Part VI, you’ll provide information that you believe will help the IRS make a decision.

Provide supporting information that you were not able to provide above.

Sign and date the form. This is a declaration, under penalties of perjury, that you believe this statement to be true, correct, and complete.

If you’re using a paid tax preparer, he or she will enter their information below your signature.

Below are some common filing considerations when requesting innocent spouse relief.

IRS Form 8857, Request for Innocent Spouse Relief, is the IRS form that one spouse can use when requesting relief from a joint tax liability that they believe to be the other spouse’s responsibility.

According to IRS Publication 971, Innocent Spouse Relief, There are three types of tax relief that a spouse may request on Form 8857:

We’ll take a closer look at each type of relief.

Innocent relief indicates that the requesting spouse is not responsible in any way for any additional tax liability, penalties, or interest arising from the actions of the other spouse. By granting innocent spouse relief, the IRS has determined that the tax liability belongs solely to the non-requesting spouse, and must only be collected from that person.

The IRS may grant innocent spouse relief if the requesting spouse meets the following criteria:

In other words, the IRS must determine that a reasonable person would not have known about the understatement of tax, and that the joint tax liability was solely the result of erroneous items that the other spouse was responsible for.

If granted, the IRS may permit tax refunds under innocent spouse relief.

Separation of liability relief is available for liabilities resulting from an understated tax. However, this relief can only apply in a situation where there is a balance due.

The IRS may grant separation of liability relief to a taxpayer under the following circumstances:

If relief is granted, taxpayer may not request a refund of additional taxes paid under separation of liability relief.

Equitable relief might be available for taxpayers who do not qualify for either innocent spouse relief or separation of liability relief.

A taxpayer may qualify for equitable relief for their tax situation if they meet the following requirements:

When considering whether to grant equitable relief, the IRS weighs the following conditions:

If granted, the IRS may permit tax refunds under equitable relief.

The IRS recommends that taxpayers apply for innocent spouse relief as soon as they become aware of a tax problem which they believe only the other spouse is responsible. However, you generally have up to 2 years from the time that the IRS first attempts collection activity for unpaid taxes to file for relief.

Here are indications that the IRS has started collection activity:

IRS Publication 971 contains more information about the time period requirements related to filing for relief.

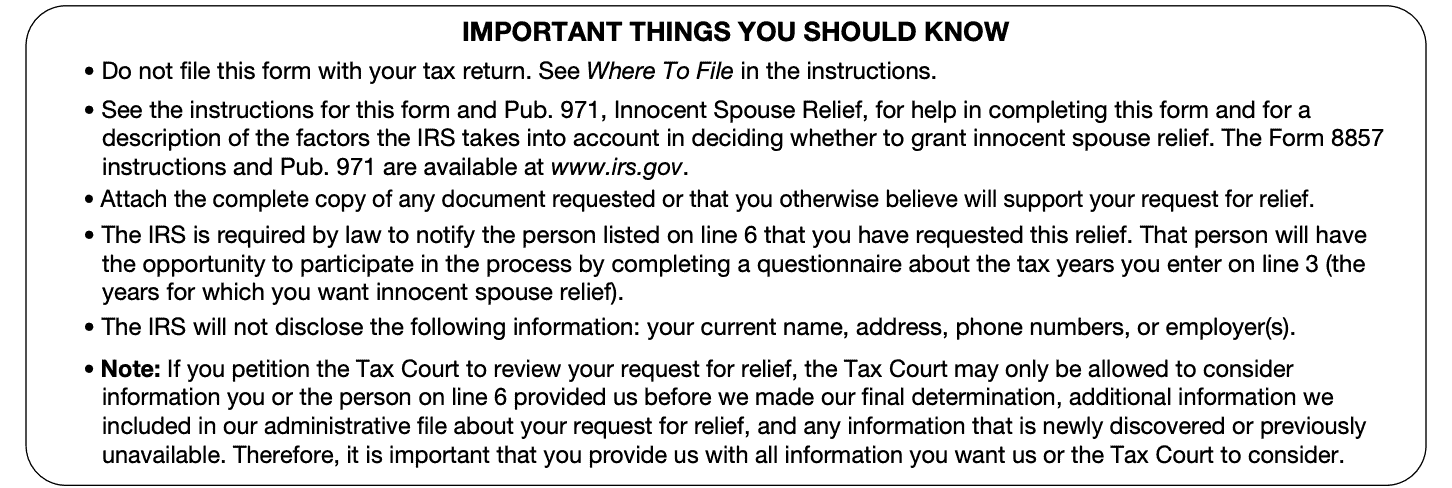

The IRS clearly states certain conditions for which a taxpayer should file Form 8857. But it also issues pretty clear guidance, on the form itself.

This is fairly straightforward. But the form instructions specifically state that you must send your Form 8857 to one of the following addresses:

Internal Revenue Service

P.O. Box 120053

Covington, KY 41012

Internal Revenue Service

7940 Kentucky Drive, Stop 840F

Florence, KY 41042

There are many factors that the IRS considers in determining whether you’re eligible for relief, or in determining the type of relief you’re eligible for. You should take some time to understand how the instructions and Internal Revenue Code apply to your financial situation before filing this form.

During your review, you might find the need to hire a tax professional. There are certain tax professionals who help their clients obtain tax relief. It might be a good idea to set up an appointment to learn more.

While you should include all required documentation, the IRS guidance also states that you cannot let this impact your timely filing of this form.

This is a very important item to consider, especially for victims of domestic violence or abuse.

While the IRS must provide the other party a questionnaire to determine their perspective, the form states that the IRS does not share the following information with the other party:

Keep this in mind as you look to apply for innocent spouse relief.

Finally, a taxpayer may petition the tax court for relief. However, the tax court can only consider the following information:

So submit your required documentation and supporting items when you apply, because there’s no guarantee that you have the opportunity to send supporting documents later on.

Watch this instructional video to learn more about how to complete Form 8857 and claim relief.

No. An injured spouse situation occurs when one spouse’s tax refund is diverted to pay the other spouse’s debt. To request injured spouse relief, you should file IRS Form 8379, Injured Spouse Allocation.

Can the IRS take my house if my husband owes back taxes?Unfortunately, yes. However, by filing for innocent spouse relief in a timely manner, you may be able to qualify for special consideration, if the federal government determines that you were not responsible for your husband’s tax mistakes.

How long do I have to file for innocent spouse relief?Generally, the spouse seeking relief has two years from the first attempt by the IRS to collect the debt to file for relief under Form 8857.

You may find a copy of this tax form on the IRS website, or by selecting the file below.